WHAT IS FRS102 (S.126) / FRS20 / IFRS2 ?

Financial Reporting Standard 102, Section 26

is the latest incarnation of the financial reporting standards relating to Share-Based Payments following on from FRS 20 and International Reporting Standard 2 (IFRS 2). All three require UK entities to recognise share-based payment transactions in their financial statements at “fair value”. The distinction between them lies in the date from which they apply.

Generally, the rules of the standards require that:

- The fair value of the share-based payment must be ascertained as at the time it is awarded;

- This fair value is then expensed to the accounts over the period in which the products or services are consumed; and

- Relevant supporting notes are provided in the accounts.

WHO DO THESE STANDARDS AFFECT ?

Whilst this may sound like a relatively straightforward question, the application date may be different for different entities and various other standards may also apply concurrently.

IFRS 2 was issued in April 2004 and for companies quoted on the London Stock Exchange it came into effect for accounting periods beginning on or after 1 January 2005.

Companies that are unlisted or listed on AIM or OFEX were not required to apply the reporting standard until accounting periods beginning on or after 1 January 2006 when FRS 20, the UK implementation of IFRS 2, came into effect.

FRS 102, Section 26 now supersedes these previous standards for accounting periods beginning on or after 1 January 2015, or 1 January 2016 for “Small Entities”.

The standards will also affect entities differently based on the nature of the share-based payment transactions in question and there are also various disclosure exemptions which is why professional guidance is often preferable.

HOW CAN EQUITY VALUE HELP ?

Equity Value has established a proven strategy

for our service of assisting companies to meet their FRS20 / IFRS2 responsibilities. This strategy is tailored to meet individual client needs. The initial stages of the process are as follows:

- Diagnosis: we establish whether the company has a disclosure requirement under IFRS2/FRS20 for the accounting period in question and also consider which share-based payments must be disclosed.

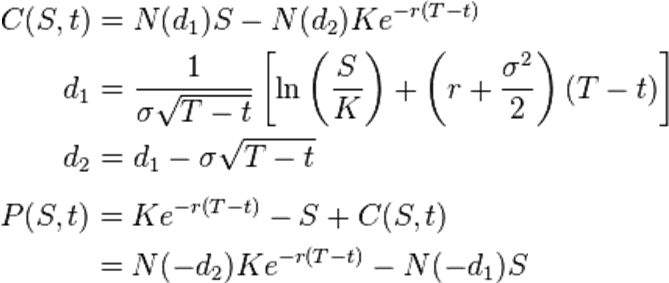

- Fair Value: we then decide on which pricing model is most appropriate. We pay detailed consideration to any relevant assumptions and then apply the assumptions and pricing model to the relevant share based payments. The result is a well thought out fair value, which we benchmark against other comparable fair values.

- Disclosure: we review the period over which relevant services are received and produce details of the requisite charges to the profit and loss account; how the balance sheet is affected including the impact on the deferred tax position and; relevant notes to the accounts.

- Report: details of all our work mentioned above is provided in a practical report that can be considered by the directors and the auditors and discussed as appropriate.

If you require any help in complying with these reporting standards, please contact us.

“All models have faults – that doesn’t mean you can’t use them as tools

for making decisions” – Myron Scholes